Healthcare

82 Mio inhabitants, 41.5 Mio working population establish a strong economy and a vital Healthcare System, which experienced a surplus of 30 billions in 2012.

It makes Germany a desirable business place no 1 in Europe.

According to the law members of the GKV (“Gesetzliche Krankenversicherung” = Statutory Health Insurance) are entitled to a sufficient, appropriate and economic standard of health care.

The actual extent of health services covered by the GBA (so called “Leistungskatalog”) is determined by the GBA (“Gemeinsamer Bundesausschuss” – Federal Joint Committee ).

The GBA is the highest decision-making body of the joint self-government of physicians, dentists, hospitals and health insurance funds in Germany. The GBA also plays the leading role in the HTA-assessment of new active substances in the so called AMNOG procedures and is therefore an institution of major significance for pharmaceutical manufacturers.

AMNOG is an abbreviation for “Arzneimittelmarkt-Neuordnungsgesetz” (Act on the Reform of the Market for Medicinal Products) a law aiming at the reform of the German pharmaceutical market that entered into force in January 2011. Main purpose was the introduction of a mandatory HTA-assessment for new active substances entering the German market as from January 2011.

The extent of health care services covered by the GKV includes generally the standard-of-care therapy for every illness (including severe and rare diseases) and certain health prevention and screening measures.

The scope of health services determined by the GBA applies uniformly to all GKVs. Therefore every person insured in the GKV receives the same level of health care regardless of the health insurances he or she has individually chosen.

Funding of the statutory health funds

The GKV funds are mostly financed by contributions that are paid partly by the members (insured) and partly by their employers. The contributions are collected by the funds but are fully transferred to a specific public health fund (“Gesundheitsfonds”). This fund also receives a fixed contribution from the federal budget.

Read more on mapbiopharma.com/germany/.

Pharmaceuticals

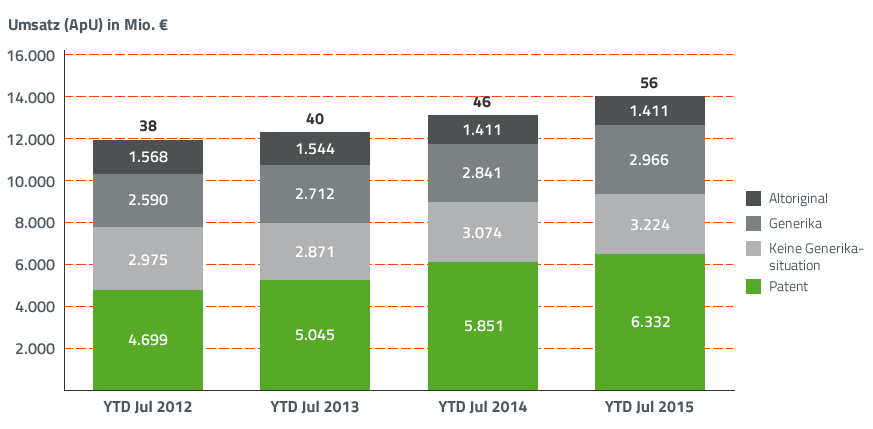

The German pharmaceutical market is the largest in Europe and the third largest in the world. The annual sales of prescribed medicinal products have a turnover of more than EUR 34 billion (2013) and this figure continues sustainable growth (+5.4% in 2013 vs. previous year).

Within Europe, Germany is the leading market for non-prescription medicines products, OTC (over-the-Counter), which may be sold only in pharmacies but for which no prescription is required.

The annual sales of self-medication products are more than € 7.3 billion (2013, with growth of +6% vs. previous year).

The largest share of the OTC medicinal products is accounted for by pharmacies with 69% (€ 5.1 billion), followed by drug stores, supermarkets and mail-order pharmacies.

The three best-selling product groups include cold remedies, gastro-, analgesics, skin products, vitamins and minerals.

[includeme file=”wp-content/data/table01.php”]

Medical Devices

Germany is the third biggest market for medical technologies in the world. German annual expenditures on medical devices and technologies amount to about € 28 billion (+2,2%). With this volume, Germany is by far the largest market in Europe.

Germany offers a broad innovation landscape with its universities and research institutes and high level lead users. Innovation and science networks offer great opportunities for new companies, 52 % of new ideas for innovative products are sourced by lead users.

Healthcare expenditure on medical devices in Germany was at around a total of € 29 billion in 2012 (source: Healthcare Expenditure Report 2012 of the Federal Statistical Office, April 2014).

€ 15.2 billion were spent on medical technical aids and € 12.8 billion on other medical services. In addition, around € 1 billion is spent on dressings and bandages, (grouped under drugs).

The Statutory Health Insurance (SHI) spends around € 17.7 billion (about 61 percent), € 6.5 billion on medical technical aids, and € 11.2 billion on other medical needs.

Source: BVMed Annual Report 2014/2015

The big amount of well-qualified doctors, scientists and engineers, as well as the high standard of clinical research give best conditions to launch new products. Numerous university hospitals and competence centres offer an extensive network in innovation and science as well as lead users.

This is resulting in short authorization processes and cost-effective clinical research. In average, it is about € 8 Mio to launch a medical device from Idea to market, vs. $ 80 Mio in US.

For medical Device Companies from US and from Japan the German market is of high interest and profitability.

Food Supplements

Germany is the largest single European market. In fact, no other European country has reached Germany’s high sales volume of OTC/Nutraceuticals. The size of the German Nutraceutical Market4) is ranging –depending on sources – between > € 950 Mio – € 1,3 billion in 2010 and 160 Mio units (7,8 % of all OTC turnover and 21,5 % units). Vitamins and mineral nutrients are dominating the market with € 500 Mio. But still the market is not saturated, as continiously new products get attention and can establish significant market Shares. German Consumers are strong believers in the organic/nature movement. Ancient famous German representatives like Paracelsus, Kneipp and Hahnemann (homeopathy) are to be mentioned.

Consumers aim for Nutraceutical products and Germans have a high affinity to organic life style. This and the high potential make Germany an important and profitable market to enter.

Recent survey (2012) initiated by the Federal Institute of Risk Assessment (BfR) asking for the intention to buy Neutraceuticals showed that the preservation of health (42%), flu and its prevention (40%), spasm (39%) and nutritional deficits (36%) were the main motivation. Other driving motivations were the intention to improve well-being, weight reduction, increased performance in sports and love life.

Top Ten Groups of Products in 2015, total market of € 739 Mio, are led by Magnesium (€ 184 Mio, 25 % market share), other minerals (€ 53 Mio, 7 % market share) Multivitamins with minerals (pregnant women) € 52 Mio, Calcium € 49 Mio, 6,7 %, Multivitamins with minerals for adults € 49 Mio, 6,7%.